While real estate professionals may be committed to their clients, clients may not always return the favor. No matter the size of a real estate business it can face potential exposures as client expectations are increasing and lawsuits are becoming more common. It is important to protect the business' financial security during a lawsuit or claim. That is why Travelers 1st Choice+® is specifically designed to offer protection to real estate professionals for the array of emerging exposures they face and can help protect the real estate firm against losses resulting from negligence, errors, and omissions in the performance of professional services. And this errors and omissions policy can be tailored to fit the business' needs. While real estate professionals may be committed to their clients, clients may not always return the favor. No matter the size of a real estate business it can face potential exposures as client expectations are increasing and lawsuits are becoming more common. It is important to protect the business' financial security during a lawsuit or claim. That is why Travelers 1st Choice+® is specifically designed to offer protection to real estate professionals for the array of emerging exposures they face and can help protect the real estate firm against losses resulting from negligence, errors, and omissions in the performance of professional services. And this errors and omissions policy can be tailored to fit the business' needs.

Learn more here.

Just like independent insurance agents, real estate agents need errors and omissions insurance. And as a BIM agent, you have access to Travelers 1st ChoiceSM for Real Estate Professionals to protect them.

Check out these product features:

-

Bodily Injury and Property Damage resulting from a covered professional service(s).

-

Disciplinary proceeding defense expenses reimbursement up to $25,000.

-

Increased liability limits available for those who qualify.

-

Defense expenses related to covered claims in additional to the limits of coverage.

-

Deductible applies to defense expenses, unless endorsed or not allowed by state.

-

Option to provide prior acts coverage without a retroactive date limitation, for those who qualify.

-

Many extended reporting period options, including an unlimited time period endorsement option.

-

No exclusion for fair-housing discrimination committed in real estate professional services as a real estate agent or broker.

-

No exclusion for losses resulting from a real estate agent or broker failing to advise a buyer or seller that pollution, fungi and bacteria exists on a property.

-

No sub-limits for certain types of claims.

-

Coverage for employees and independent contractors of the insured automatically included as protected persons for claims resulting from professional services they perform for the named insured.

Check out these flyers and checklists to help you sell coverage to your clients.

Need Realtor® prospects or contact information for a Realtor you know? Try the "Find a Realtor" feature. Call five a day and you'll be homing in on sales in no time! Coverage is available in all states with the exception of CA, HI, and LA and is written on admitted paper. Log in to Big "I" Markets at www.bigimarkets.com and click on Real Estate Agents and Property Manager E&O to learn more or to request a quote.

|

SPECIAL FEATURE

Risky Business

Insuring the Marijuana Industry

By Julie Carter By Julie Carter

The number of states legalizing the growth, distribution and possession of marijuana, in one form or another, continues to increase. As of this writing, twenty-eight states and the District of Columbia have legalized the use of medical marijuana; eight states and the District of Columbia have legalized the use of recreational marijuana. The cannabis market is a multi-billion dollar industry, with revenue expected to reach $20 billion by 2021. It is important to remember, the fact is that the growth, distribution or possession of marijuana is a crime under federal law.

As with any other business, those involved in the industry are seeking insurance coverage for their assets and potential liabilities, and the opportunities for carriers, brokers and agents may seem endless. To continue on to the full article click here.

Log into the Big "I" Professional Liability Risk Management Web site, EOHappens at www.iiaba.net/EOHappens to access more Big "I" member-exclusive content for your agency.

Julie Carter is an assistant vice president, claims specialist with Swiss Re Corporate Solutions and works out of the office in Overland Park, Kansas. Insurance products underwritten by Westport Insurance Corporation, Overland Park, Kansas, a member of Swiss Re Corporate Solutions.

|

AIG for Affluent Multinational Homeowners

High-net worth people may maintain residences around the world. There are many reasons to do this. Some do it as a real estate investment. Others vacation or do business in foreign countries and prefer a place of their own over a hotel. High-net worth people may maintain residences around the world. There are many reasons to do this. Some do it as a real estate investment. Others vacation or do business in foreign countries and prefer a place of their own over a hotel.

These places need to be furnished and maintained and that can mean a fairly large investment alone, especially in some of the world's great shopping areas. Even if a piece is purchased to bring back to the U.S., there may be export problems, which might mean an expensive piece must remain behind or be seized. Another consideration is liability issues. If your client has an auto accident in Europe, what happens next depends on in which country it takes place. Having someone to rely on that understands the complexities of world travelling high-net worth individuals and families can put their minds at ease.

Big “I” Markets agents have access to AIG's Private Client Group, which offers multinational protection for your clients' global lifestyle with:

-

A single point of contact

-

A simpler approach to complex property coverage

-

Consistent claims support

-

Platinum Account coordination (for those that meet U.S. requirements)

AIG's Private Client Group homeowner coverage is available for dwelling replacement cost coverage valued at $500k or more in most states.

Included are:

-

Guaranteed replacement cost - Included

-

Back-up of sewers and drains - Included; up to dwelling value

-

Business property - Up to $25,000

-

Deductible options - Up to $100,000 available

-

Primary flood - Available

-

Equipment breakdown - Available

-

Identity fraud restoration expenses, ATM robbery, and financial fraud, embezzlement or forgery - Available

-

Traumatic threat or event recovery - Available

-

Green rebuilding expenses - Available

-

Waiver of deductible on losses over $50,000 - Available

-

Replacement cost cash out option - Included

-

Lock replacement - Included; no deductible

-

Food spoilage - Included

-

Loss prevention devices following a claim - Included; up to $2,500 available

AIG's Private Client Program and is available to registered members in all states. Travel over to Big "I" Markets and click on Affluent Program - New Business to learn more!

|

| |

Remember that you can view the following webinars 24/7 by checking out the BIM Webinar Library. To do that log onto Big "I" Markets and click on "Publications".

-

AIG Private Client Group Homeowner - Collections CoverageNEW

-

Chubb Masterpiece Homeowner - Overview NEW

-

CBIC Architects & EngineersNEW

-

AIG Private Client Group Homeowner - Automobile NEW

-

AIG Private Client Group Homeowner - Overview NEW

-

TravPay

-

Commercial Lessor's Risk

-

Affluent Homeowners

-

Travel Insurance

-

Community Banks

-

Affluent Homeowner

-

Real Estate E&O

-

RLI Personal Umbrella

-

"Oh, by the way...Flood Sale"

-

Habitational

-

Student Housing

+++++

BIM WEBSITE TRAINING WEBINAR

For all you folks who recently registered for Big "I" Markets, remember you can participate in a webinar from the comfort of your office to help you learn how to navigate around the system. Every Thursday at 2:00 p.m. EDT we'll show you how to navigate the Big "I" Markets platform, including how to submit a quote! A recording of this webinar can be found under "Publications" after logging into Big "I" Markets.

+++++

Big "I" Product Webinars

-

NEW - Wednesday, June 7 @ 2:00 - 3:00pm EDT. "Chubb International Advantage - Foreign Package Policy Webinar". Placing appropriate coverage for foreign exposures can sometimes be challenging. Please join us and Brandon Boyd of Chubb Multinational Property and Casualty for a 45 minute webinar on how a comprehensive foreign package policy offers protection for businesses, employees, independent contractors, volunteers, students and more while traveling or doing business outside of the United States. Topics will include an overview of international insurance basics along with tips on identifying gaps left by domestic coverage for foreign exposures, ways to identify overseas risks by asking clients key questions, top classes of business that have overseas exposures and international claims scenarios that will help emphasize the importance of a foreign package policy.

Register here Cost: Free.

+++++

Big "I" Virtual University Webinars

Don't miss the following education opportunities provided from the Big "I" Virtual University experts that focus on topics agents need to know to make a smart start in 2017. For more information, contact national staff.

Other topics in the 2017 schedule cover partial losses, contractual risk transfer, business income, contractors and more. The entire schedule, including registration links can be found online here.

-

Wednesday, June 14 - 1:00 - 3:00pm EDT. "Untangling the Work Comp Mess - When Employees Travel and Their Families Sue". When employees travel out of state for work, real work comp coverage gaps can exist; and these gaps could leave the employer without the necessary protection they THOUGHT they purchased when they paid their work comp premiums. Extraterritoriality and reciprocity are major work comp problems most agents don't know they have. Yes, every state provides extraterritorial work comp protection, but not every state recognizes that coverage – so many insureds are unknowingly blindsided by uncovered or improperly covered claims.

Some agents take Part II – Employers' Liability coverage for granted. They consider it just a "thrown in" coverage with no real benefit. But Employers' Liability protection fills major gaps between the work comp policy and the CGL. Without this important coverage, your insured could have a hefty out-of-pocket expense.

Attendees to this session learn:

-

What "extraterritoriality" and "reciprocity" are in relation to work comp;

-

How limitations in some state reciprocity laws create major gaps in work comp coverage;

-

How to fix these coverage gaps; and

-

Why employers' liability coverage is so extremely important.

Click here to register. Cost: $69

|

STUDENT OF THE INDUSTRY PARTING SHOT

Accident Year Loss Ratio: The Cool Kids at Insurance School

By Paul Buse, President of Big I Advantage®

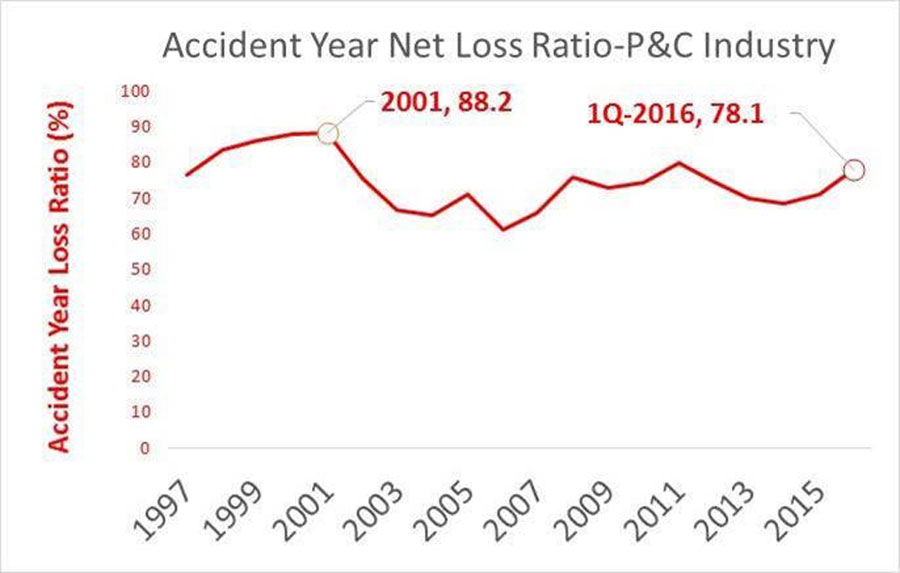

Recently I received the 1Q results for our fair industry as summarized by ALIRT Insurance Research. "1Q" being finance-speak for the first quarter of the year. I was jarred by the accident year combined ratio: One-O-Six (106%). The folks at ALIRT use a basket of insurers they follow closely to make these quick assessments as we go through the year. At Big I Advantage® we use ALIRT to help us track both the insurers we are appointed with and the industry in general. Oh, they attributed the results to "very high catastrophe losses from severe thunderstorm and convective weather events in March especially." Convective Events are also known as big thunderstorms and resulting hail and tornados.

Anyway, losing 6 cents on each premium dollar when interest rates are low is sure to get the attention of insurer CEOs. To give you some sense of 106, I stripped out the approximate 28% expense ratio to get to the 78.1% accident year loss ratio. Then I juxtaposed the Accident Year Loss Ratio equivalent to that 106 "combined" with industry accident year loss data back to 1997. As you can see even our first quarter of 2017 is still 10 points below the industry results in 2001 but it's above most years in recent past and, of course, a quarter doesn't make a year.

Click for larger version

Source: Schedule P for 1997 to 2016 Accident Year Loss Ratios and ALIRT Insurance Research for 1Q 2017 estimate

Why are Accident Year Loss Ratios the "cool kids" at insurance school? Because they tell you the grittier version of the story than what you often get…unfiltered from generalizations from parental-like accountants. There is no including distracting loss reserve changes from past years in these. Unlike Calendar Year Loss Ratios, Accident Year Loss Ratios are closer to the "feeling" of a year with losses matched most closely to the premiums during the same time period. If you want the full ALIRT report for 1Q, email me and I'll send it your way.

|

BIG "I" MARKETS SALE OF THE WEEK

Congratulations to our agent in Washington on an Affluent Homeowner sale of $35,997 in premium!

|

|