What Makes a Risk Insurable?

One of the most important early concepts you will learn in insurance is this: What makes a risk insurable? This article helps to explain the elements of an insurable risk.

What makes a risk insurable, especially in today’s hard market with volatile climate risks seemingly escalating?

What is an Insurable Risk?

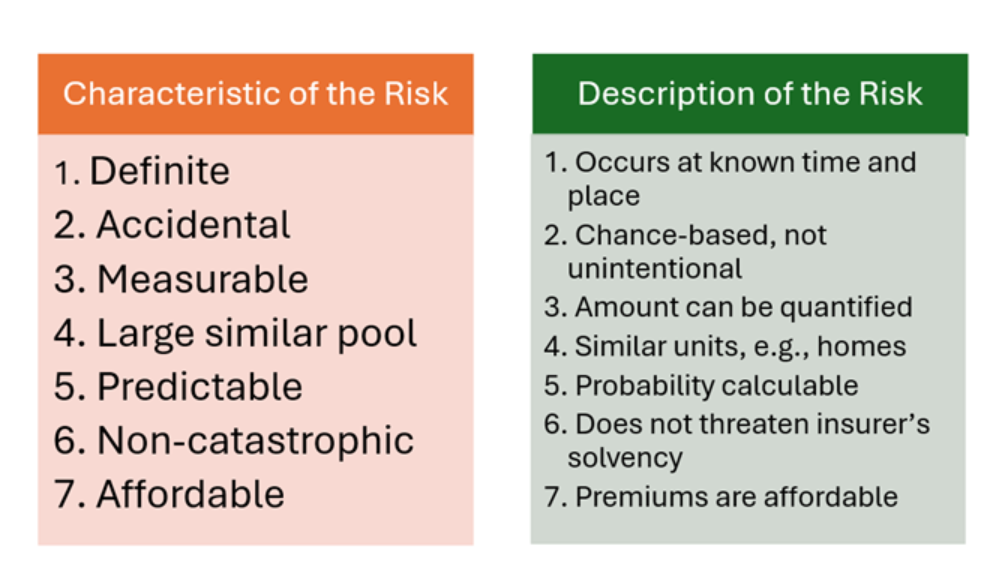

- There must be a large pool of dispersed similar exposure units. Additionally, the insurer must have access to or develop realistic loss data to better predict future loss costs based upon this historical data. Consider a large pool of Florida homes, for example. The law of large numbers, a statistical tool that helps actuaries predict future losses, helps make these future loss predictions more valid. According to the law of large number, the greater the number of aggregated similar exposure units and historical loss data, the greater underwriters’ and carrier senior managements’ confidence is in predicting future losses. These predictions help to ensure accurate pricing.

- The perils covered by the policy should be random and unplanned to your insureds. In other words, losses should be accidental. This is why virtually every property or casualty policy has an exclusion for “intentional acts,” for example. The premise of insurance is to insure against unplanned perils.

- Adjusters must be able to measure losses to properly pay claims. In property coverage, these are tangible losses such as roof damage or flood residues. Some indirect losses such as losing access to an insured property are also considered insurable because they arise out of the loss itself. However, intangible losses like criminal behaviors are more difficult to measure and therefore not insurable. It is not the intent of insurance to cover these types of intentional acts.

- There should be a large similar pool of like units. Consider coverage for long-term elder care. In the 1980s, underwriters were just exploring how to price nursing homes. I recall talking to one surplus lines underwriter who said they were using “Seat of their pants” estimations for how to profitably write nursing homes. As the U.S. population ages; however, in 2024, there were 66, 630 long-term care facilities under regulation in the U.S. Therefore, as more loss data develops from nursing home claims, the more predictably actuaries can estimate adequate yet not inflated premiums.

- Losses should be predictable. That means actuaries can gather enough information from past losses to adequately predict premiums. Given abnormally unpredictable weather, you might better understand why this is challenging today’s insurers.

- Losses should be non-catastrophic. Wildfires are increasingly a topic among states experiencing heavy fires, especially in areas with a large population in wildland urban interface (WUI). The U.S. Fire Administration defines WUI as “…the zone of transition between land and human development. It is the line, area, or zone where structures and other human development meet or intermingle with undeveloped wildland or vegetive fuels.” Flood, too, can be widespread and catastrophic. Hence, the unendorsed homeowners policy does not cover flood damage.

- Based on the elements in the diagram below, can the insurer cover the loss at a profitable premium? An affordable premium is an incentive for your clients to transfer their risk. As the cost of premiums rises, so does your insured’s reluctance to buy adequate coverage (which of course, increases your chances of an errors & omissions claim). In today’s world and according to John Putnam, an expert in wildfire risk, this affordability is subjective.

Explaining These Principles to Your Insureds

There may be times your insured asks for coverage, and you are unable to find a carrier to assume the risk. This chart can help you understand why the underwriter declined the risk. In some cases, there may be no alternative. You may not have a market, or in fact, the risk may be so new that no insurance markets have responded to write that type of risk.

Consider the first decriminalization of cannabis in Oregon in 1973. At that time, surplus lines insurers saw an opportunity, and 2016 saw at least five states balloted pro-cannabis legislation. Since then, cannabis insurance availability is widespread as underwriters more widely embraced cannabis risks.

The chart below outlines the characteristics and descriptions of insurable risks.

Conclusion

Whether you are new to the industry or facing hard market challenges, it is fundamental to understand what makes a risk insurable. The seven key elements — from the need for a large pool of similar exposure units to the importance of non-catastrophic and measurable losses — are the foundation for deciding whether an insurer will cover a risk. These principles not only guide underwriters and actuaries in pricing and managing risks but also help insurance professionals explain coverage limitations and premiums to their clients.

As the world evolves, with challenges like climate change, unpredictable weather, civil unrest and emerging risks such as plastics contamination and space junk, the criteria for insurability continue to be put to the test.

However, knowing that your underwriters adhere to these foundational principles, insurance agents can better understand coverage declinations and can strike a balance between the agency’s profitability and reputation and providing meaningful protection to their clients.

Copyright © 2026, Big “I” Virtual University. All rights reserved. No part of this material may be used or reproduced in any manner without the prior written permission from Big “I” Virtual University. For further information, contact nancy.germond@iiaba.net.