Verisk to Roll Out New General Liability Exclusions for Generative AI Exposures

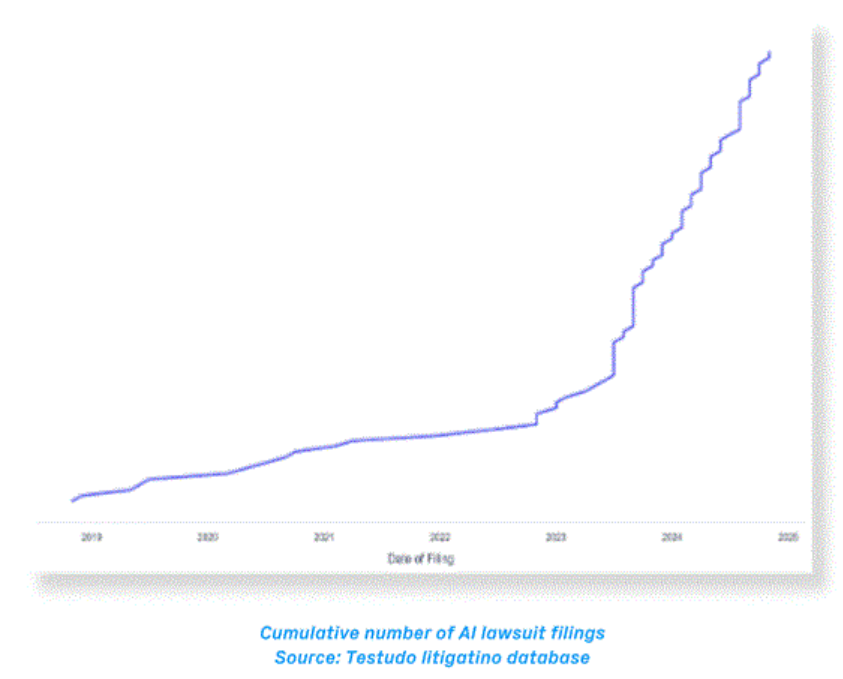

Generative artificial intelligence (AI) is transforming how the insurance industry does business. However, it’s also triggering a wave of legal and insurance challenges. With at least 11 major lawsuits currently underway in the U.S., ranging from copyright infringement to harmful chatbot interactions, insurers are addressing the growing risks associated with this technology.

From copyright infringement to image generation problems, these cases highlight the importance of an organization’s need for insurance protection when using generative AI.

According to a recent Bain & Company report, which describes generative AI’s “soaring” use, 95% of U.S. companies currently use generative AI. Calling generative AI a “business staple,” the report states that “accuracy concerns are beginning to ease” as more companies gain confidence in gen AI’s outputs.

This confidence, however, can produce liability issues as more companies rely on—and perhaps distribute—generative AI content that is faulty. In one tragic example from last year, the parents of a child who died by suicide filed a lawsuit alleging that information furnished by a generative AI chatbot contributed to the child’s death.

In healthcare, concerns are mounting over attacks that could corrupt medical data. Generative AI, while powerful, is proving to be a double-edged sword.

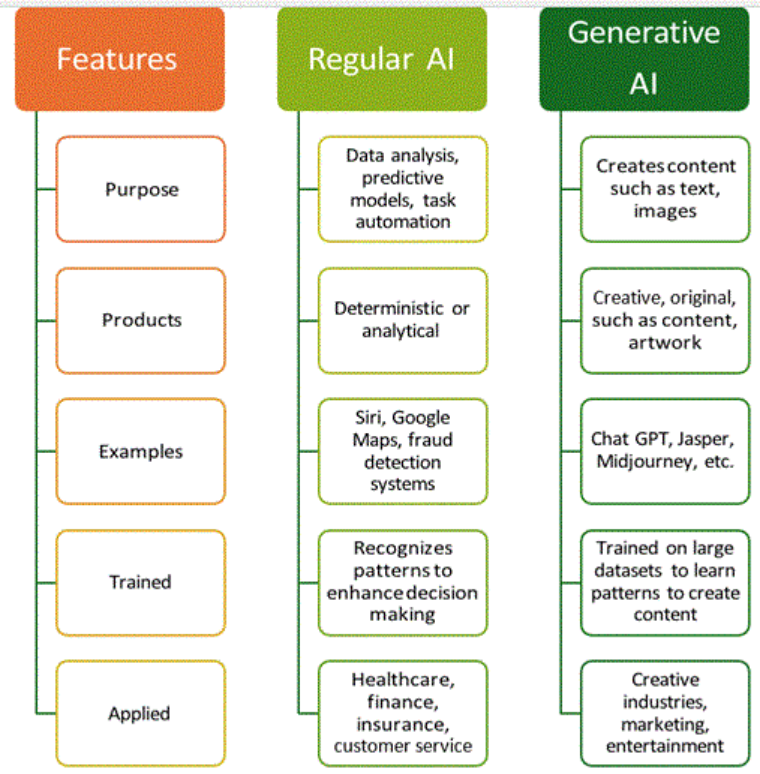

Differences Between AI and Generative AI

Regular AI focuses on processing data and making decisions. In contrast, generative AI creates new content, such as text, images, audio, video or code based on training data. These distinctions are critical when assessing the need for accurate insurance coverage.

How Verisk Has Responded to the Gen AI Trend

In response to the rapidly developing Gen AI exposures, insurers requested underwriting tools to address this emerging risk. Verisk’s ISO Core Lines and Emerging Issues teams developed new general liability endorsements that allow carriers to exclude generative AI exposures.

Effective January 2026, these exclusionary forms provide insurers with the ability to “generally exclude this emerging exposure,” according to Verisk.

The following forms define gen AI as follows.

“Generative artificial intelligence” means a machine-based learning system or model that is trained on data with the ability to create content or responses, including but not limited to text, images, audio, video or code.”

Verisk based this definition on “existing definitions provided by government sources and NAIC definitions.”

Here are descriptions of the forms with a January 2026 edition date. Verisk has already received great interest from carriers and expects that insurers will quickly roll out these exclusions based on that interest.

Here are some of the key exclusions.

- CG 40 47 Exclusion – Generative Artificial Intelligence (for use with the ISO Commercial General Liability Coverage Part. For use with both the occurrence and claims-made versions, this optional endorsement excludes coverage under Coverage A and Coverage B with respect to bodily injury, property damage or personal and advertising injury arising out of generative artificial intelligence.

- CG 40 48 Exclusion – Generative Artificial Intelligence (Coverage B). For use with the ISO Commercial General Liability Coverage Part, both the occurrence and claims-made versions, this optional endorsement excludes coverage under Coverage B with respect to personal and advertising injury arising out of generative artificial intelligence.

- CG 35 08 Exclusion – Generative Artificial Intelligence. For use with the ISO Products/Completed Operations Liability Coverage Part, this optional endorsement excludes coverage under Section I with respect to bodily injury or property damage arising out of generative artificial intelligence.

Some surplus lines carriers have already deployed AI exclusions, and regulators are creating regulations for high-risk and specific-use cases of gen AI.

For example, Berkeley has rolled out an absolute AI exclusion that excludes “…any actual or alleged use, deployment, or development of Artificial Intelligence by any person or entity, including but not limited to: a) the generation, creation or dissemination of any content or communications using Artificial Intelligence.”

Filling the Gap: New Coverage for Gen AI Liability Exposures

When exclusions arise, new markets open. As with any new invention or product that creates an insurable risk, the insurance market, with its entrepreneurial spirit, responds.

Testudo saw the need for a specialist product to cover generative AI liability exposures and will launch as a Lloyd’s cover holder. They created this product to provide policyholders with financial protection in light of incoming generative AI exclusions in commercial general liability and sharp increase litigation.

Testudo’s claims-made policy form will cover the following gen AI exposures.

- Generative AI errors: Financial loss suffered by a third party due to negligent acts, errors, omissions, misstatements, or misrepresentations arising from AI outputs.

- Intellectual property infringement & defamation: Legal claims related to defamation, libel, slander, trademark violations or copyright infringement caused by AI outputs.

- Bodily injury. Liability for injuries resulting from reliance on, or interaction with, AI-generated outputs.

- Property damage. Liability for damage caused by reliance on, or interaction with, AI-generated outputs.

- Unauthorized data disclosure: Liability for unintentional disclosure of protected information through inclusion in AI outputs.

Testudo also offers the following risk mitigation tools:

- AI exposure reports to enable brokers to highlight generative AI liability exposure for their clients.

- AI litigation monitoring to stay on top of moving AI liability trends.

Testudo expects strong demand for this coverage from companies that integrate vendor generative AI systems into their operations. Examples include customer service chatbots or generative AI systems to automate tasks within an organization.

However, Testudo will not yet underwrite generative AI developers and vendors that sell their technology products as a service because they are covered in traditional insurance policies such as technology errors & omissions. Further, Testudo will not underwrite developers and vendors that customize or modify foundational AI models to create a specific generative AI system or application.

Testudo’s policy will not include invasive, time-consuming audits, and they are actively partnering with agencies ahead of their launch at the end of 2025. Testudo co-founder, George Lewin-Smith, predicts strong demand for their produce as a result of Verisk’s exclusions. “We believe that 95% of carriers will immediately employ these exclusions,” he said.

Interest in incorporating the exclusions is already strong from carriers, according to Verisk personnel, who also predict rapid adoption of the new exclusions.

To meet the challenges surrounding AI, some surplus lines carriers have already implemented generative AI exclusions. For example, Berkeley introduced an absolute exclusion that bars coverage for any use, deployment or development of AI, including content generation. Munich Re and Armilla—a Lloyd’s Coverholder—have also introduced generative AI coverage, signaling a broader industry shift.

It’s clear that generative AI is not just a trend; it has become a key driver of efficiency in the majority of U.S. businesses.

Copyright © 2026, Big “I” Virtual University. All rights reserved. No part of this material may be used or reproduced in any manner without the prior written permission from Big “I” Virtual University. For further information, contact nancy.germond@iiaba.net.