Calculating the Insured’s Lowest Possible Work Comp Mod

Once the mystery is removed from the experience mod worksheet, development of the lowest possible experience mod is quite easy. This article shows how to develop the lowest possible mod while at the same time highlighting the fact that achieving this mod may not have the intended result.

|

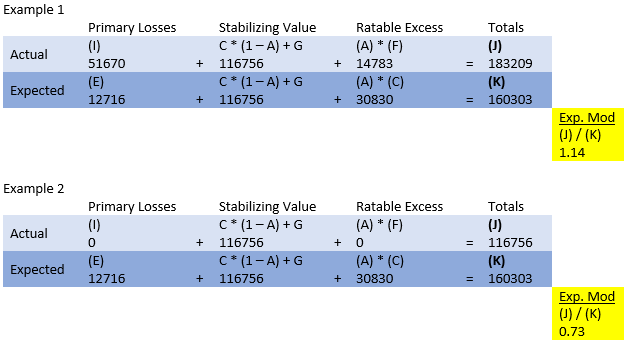

Once the Workers’ Compensation Experience Modification worksheet is understood, dare I say, mastered, calculating the insured’s lowest possible experience mod is easy. In fact, it’s ridiculously easy. Simply “zero out” all actual losses. Remember, NCCI’s experience mod calculation is: Following is a demonstration using actual, though completely fabricated, values. The first example presents a mod with actual losses included, and Example 2 has no actual losses (so the lowest mod can be developed).

When developing the lowest mod, the agent and the client must remember four key caveats:

Knowing the lowest possible mod and the key caveats to calculating and achieving it allows the insured to make a business decision regarding how to manage its workers’ compensation program. The insured must decide if the benefits of achieving the lowest possible mod are worth the time, effort and possible investment. And even if the lowest mod is achieved, the underwriter may negate the effort by removing credits or debiting the account.

Last Updated: May 26, 2017 |

If boxes (I) and (F) are “0” (no actual losses), the total in box (J) equals the stabilizing value. With the “Actual” row (the top row) limited to the stabilizing value and the “Expected” row, (K), developed as normal, the result is the insured’s lowest possible experience mod.

If boxes (I) and (F) are “0” (no actual losses), the total in box (J) equals the stabilizing value. With the “Actual” row (the top row) limited to the stabilizing value and the “Expected” row, (K), developed as normal, the result is the insured’s lowest possible experience mod. The lowest possible experience mod for this insured is 0.73.

The lowest possible experience mod for this insured is 0.73.Copyright © 2026, Big “I” Virtual University. All rights reserved. No part of this material may be used or reproduced in any manner without the prior written permission from Big “I” Virtual University. For further information, contact nancy.germond@iiaba.net.